Tax Withholding From Pension

Your pension payer must withhold federal income tax from your monthly benefit unless you submit IRS Form W-4P with a valid exemption. If you don’t provide a W-4P, the payer will use a default rate: single filer with zero allowances, which results in a flat 10% withholding on each periodic payment. You can change this rate at any time by filing a new W-4P with your plan administrator.

The goal is to match your total withholding to your actual tax liability—avoiding a large bill in April and preventing an interest-free loan to the IRS. But the rules shift depending on payment type, rollover status, and whether you have other income sources. Below we cover how the system works, the one mistake that catches most retirees, and a fast way to verify you’re on track.

Applicability boundary: The rules described here apply to employer-sponsored qualified pension plans (defined-benefit and defined-contribution plans subject to ERISA). If you have a nonqualified deferred compensation plan, an IRA, or an annuity from an insurance company, the withholding rules may differ. For pensions from foreign employers, consult a tax professional familiar with cross-border rules.

How Federal Withholding Works for Pension Payments

Pension distributions are fully taxable unless you made after-tax contributions (rare in most employer plans). Federal income tax withholding is elective for periodic payments, but the plan defaults to a 10% rate if you don’t act. For lump-sum distributions not rolled over into an IRA, a mandatory 20% withholding applies (IRS Publication 15-A).

What this means for you in practice: If your total tax liability is less than 10% of your pension (e.g., you have large deductions or are in the 0% bracket), you are over-withholding—giving the IRS an interest-free loan. If your liability is higher (e.g., you have a part-time job, investment income, or taxable Social Security), you risk underpayment penalties. The immediate action is to calculate your expected effective tax rate and adjust your W-4P accordingly. Don’t assume the default 10% is correct.

Key numbers to know:

- Periodic payments (monthly, quarterly): Default 10% when no W-4P is on file.

- Nonperiodic distributions (lump sum, partial cash-out): Mandatory 20% federal withholding if taken as cash; can be avoided only by a direct rollover to an IRA or another qualified plan.

- Required minimum distributions (RMDs): Withholding is optional; you can request any amount or choose “no withholding” by filing a valid W-4P.

If you are a married couple, you may elect a lower withholding rate (even zero) when you both sign the W-4P certifying that your total tax owed will be covered by other payments or credits. This is the trade-off: electing zero withholding increases your monthly cash flow but can trigger underpayment penalties if you don’t make estimated tax payments equal to at least 90% of your current year’s tax or 100% of last year’s tax (110% if your prior-year adjusted gross income was over $150,000).

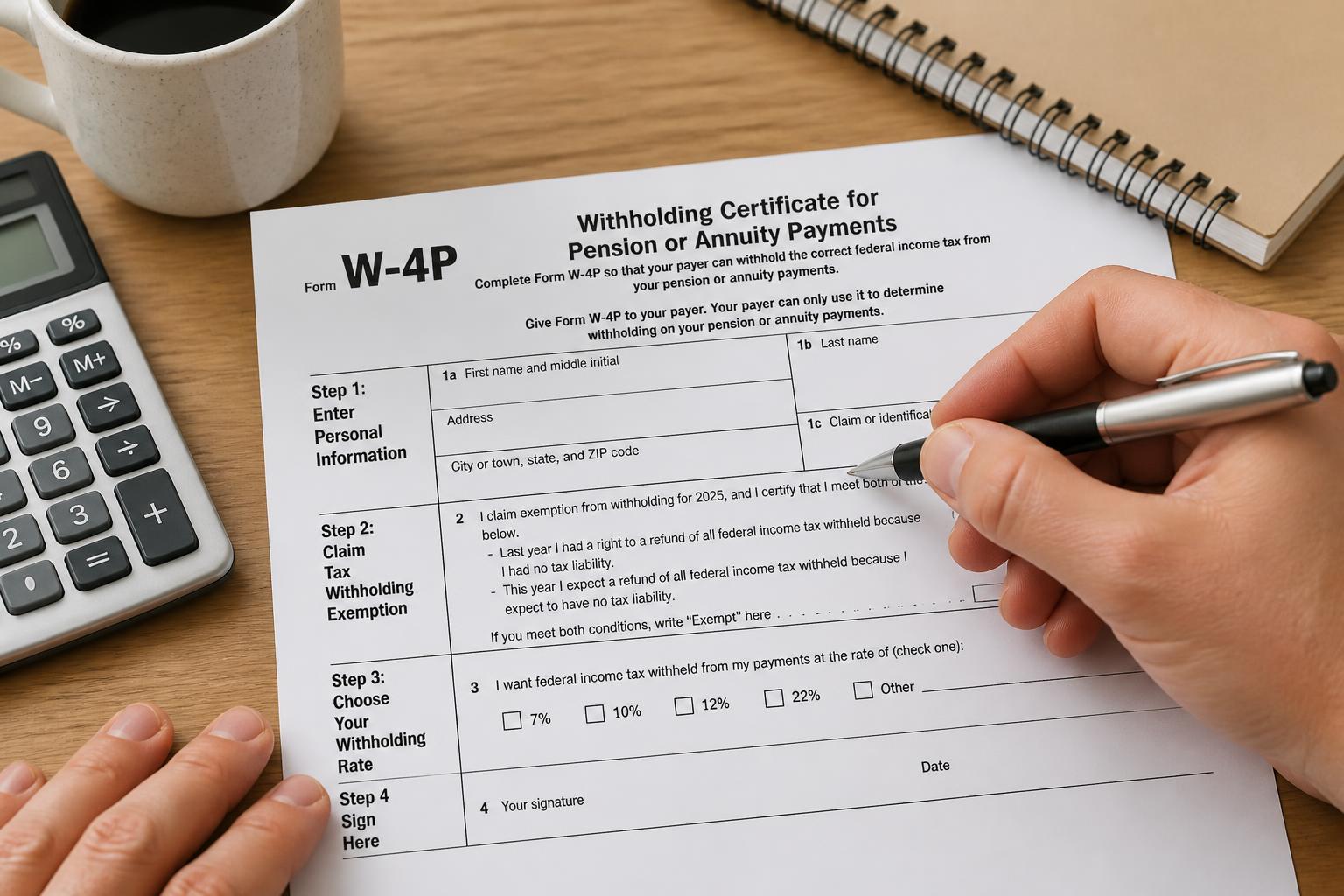

Choosing Your Withholding Rate with Form W-4P

Form W-4P works like the W-4 for wages but is specific to pensions and annuities. You specify:

- Filing status (single, married filing jointly, head of household)

- Number of allowances (typically “0” unless you have dependents or large deductions)

- Additional flat-dollar amount to withhold per payment

Example: A retiree with a $2,500 monthly pension who also has a part-time job earning $1,000/month can add $75 per month on Line 4 of the W-4P to cover taxes on the extra income without touching the pension’s base rate.

Common mistake: Relying on last year’s W-4P after a marriage, divorce, or change in Social Security taxation. The IRS Tax Withholding Estimator (irs.gov) can recalculate your ideal withholding in about 10 minutes.

Verification step: Log into your pension provider’s online portal and look for your current withholding election. If you see “Single, 0 allowances” and you haven’t updated it recently, you are on the default 10% rate. To confirm your actual withholding percentage, divide the amount withheld on your most recent payment by the gross pension amount. If the result is not what you expected, update your W-4P.

The One Failure Mode That Trips Up Most Retirees

The most common mistake is failing to account for the taxability of Social Security benefits. Up to 85% of your Social Security income can be taxable when combined with pension income. The W-4P only covers the pension itself—it does not automatically adjust for SS benefits. If you ignore this, you may end up under-withheld by $1,000–$3,000 per year.

How to detect it early: Each September, run the IRS Tax Withholding Estimator with both your pension amount and your estimated Social Security benefit (use the amount shown on your SSA-1099 from last year). If the tool shows a projected underpayment of $1,000+ and you are not already making estimated tax payments, update your W-4P immediately with additional withholding.

Expert Tips for Getting Withholding Right

Tip 1: Set a calendar reminder to review every October.

The IRS releases updated withholding tables each year. Even if nothing else changes, the tax brackets are adjusted for inflation. A simple 15-minute check using the IRS Tax Withholding Estimator can catch a drift.

Common mistake: Assuming last year’s settings still work. Tax law changes (like the SECURE Act 2.0 RMD age shift) can affect how much you owe.

Tip 2: If you have multiple retirement accounts, treat them as one portfolio.

A pension plus IRA withdrawals plus a part-time job means each payer only knows its own piece. Instead of trying to split withholding evenly, choose one account (usually the pension) to carry all the extra withholding needed for the combined income.

Common mistake: Relying on each payer to withhold “just enough” individually—this almost always leads to under-withholding.

Tip 3: Use state withholding forms for the 14 states that tax pension income.

Federal withholding has no effect on state tax. If you live in Minnesota (Form M-W4P), Oregon (Form OR-W4P), or California (DE 4P), you must file a separate state withholding election with your pension payer. Some plans also have their own state-specific forms.

Common mistake: Assuming federal Form W-4P covers state taxes. It does not. Check your state’s tax website or call your plan administrator.

Verification Checklist

Run through these five items now to confirm you’re on track:

1. Form W-4P on file? – If you never submitted one, your payer is defaulting to a 10% single rate, which may be too low or too high for your situation.

2. Filing status correct? – Married retirees who both receive pensions often need “married filing jointly” with the correct allowance count. A common error is using “single” or “married but withholding at single rate” when it doesn’t match your return.

3. Other income included? – Did you add extra withholding for part-time work, investment dividends, or self-employment? If you rely only on the pension base rate, you could be short.

4. State withholding arranged? – If you live in a state that taxes pension income (e.g., California, Oregon, Minnesota), you need a separate state withholding form. Federal withholding does not cover state taxes.

5. Annual review scheduled? – Update your W-4P every October, when the IRS releases new withholding tables, or after any major life change (marriage, divorce, death of spouse, significant increase in SS benefits).

Action step: Open the IRS Tax Withholding Estimator at irs.gov/individuals/tax-withholding-estimator. Enter your pension amount, other income, and Social Security estimate. The tool will recommend a number of allowances and any extra withholding.

Quick Reference: Default Withholding Rules

| Payment type | Default if no W-4P | Can you reduce or waive? |

|---|---|---|

| Monthly/quarterly pension | 10% (single, 0 allowances) | Yes—file W-4P to change rate or claim exemption |

| Lump-sum cash distribution | 20% mandatory | Only by direct rollover to IRA or another plan |

| RMD | No default with W-4P; payer may assume 10% | Yes—file W-4P to set any amount |

If you take a lump-sum distribution without a direct rollover, the 20% withholding is required even if you plan to reinvest the money later. Be sure you understand this before you request a cash payment.

When to Seek Professional Help

The information above is for educational purposes and is not tax or legal advice. Consult a CPA or enrolled agent if:

- Your income exceeds $100,000 and includes multiple streams (pension, Social Security, IRA withdrawals, rental real estate).

- You are subject to the Net Investment Income Tax (3.8% surcharge) or the Additional Medicare Tax.

- You live in a community property state (CA, TX, WA, etc.) where pension withholding rules differ for married couples.

- You are considering a partial lump-sum buyout offer from your pension plan—the withholding and rollover options can be complex.

Review your latest pension statement for the withholding amount and compare it to your prior-year tax liability. Adjust your W-4P if needed. For state-specific forms, visit your state’s department of revenue website.

Explore This Topic

- Back to Us State Pension Tax

- Back to Us State Pension Tax

Related guides in this cluster:

Michael Reynolds is a retirement benefits researcher and the lead author at Pension FAQ. With over 12 years of experience analyzing employer pension plans, state retirement systems, and Social Security policy, he specializes in translating complex pension rules into clear, actionable guidance for American workers and retirees.

Michael holds a Bachelor’s in Economics from the University of Michigan and has completed the Certified Retirement Counselor (CRC) program. His work has been cited by financial planners and HR professionals helping employees navigate their pension options.

At Pension FAQ, Michael leads a team covering employer plan access, state pension taxation, teacher and public employee retirement systems, professional sports pensions, and pension calculation rules. All content is rigorously reviewed against official plan documents and IRS guidelines.

Disclaimer: Pension FAQ content is for educational purposes only and does not constitute financial, tax, legal, or retirement benefits advice. Always consult your plan administrator or a qualified professional for decisions about your specific situation.